Is stock analyst coverage too “crowded?”

The most-covered 5% of U.S. equity account for more than 25% of analyst coverage.

Investors rely on equity analysts to “crunch” large volumes of data from firm financial statements, press releases, or social media. Analysts take this raw information and turn it into trading signals such as earnings forecasts and stock recommendations. In this way, analysts help investors learn about a company’s future prospects.

However, it is much easier to learn about some stocks than about others. The most-covered 5% U.S. equities account for more than 25% of analyst coverage. In the last quarter of 2017, companies such PayPal (42 earnings forecasts), Amazon (39), and Netflix (32) occupied the spotlight. By comparison, the median S&P 1500 has only four earnings forecasts. Even more, eighteen firms in the S&P 500 universe had no earnings coverage at all.

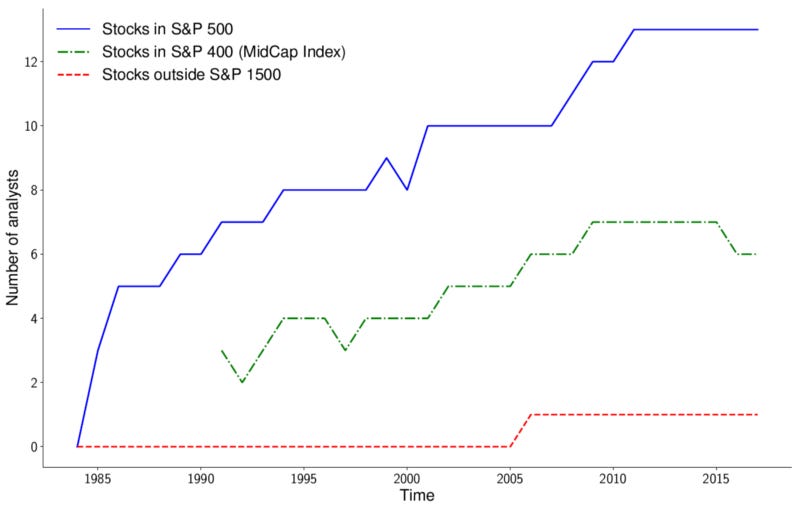

The coverage gap seems to grow larger over time. The median stock outside the S&P 1500 index had no earnings coverage before 2006, and only a single forecast per quarter between 2006 and 2017. In contrast, S&P 500 stocks coverage increased four-fold over the past three decades: from three analysts in 1985 to 13 in 2017.

Why does coverage “crowd” in some stocks? One argument is that investors want it that way. Investors have, after all, a limited attention span. They cannot equally learn about, say, all S&P 500 stocks and might prefer analysts to focus on the likes of Netflix and Amazon. For example, because a large share of intangible assets makes it difficult to evaluate such companies by themselves. In this case, analysts therefore simply cater to what their target audience wants.

At the same time, crowded coverage could be a symptom of market inefficiency and resource mis-allocation. Analyst brain- and computer- power are limited. They should be judiciously allocated across stocks to achieve the highest informational gain for investors. Is the marginal benefit from the 40th Amazon earnings forecast larger than having at least one forecast for CBS Corporation? After all, investors hold diversified portfolios. Wouldn’t they also prefer diversified coverage?

I tackle this question in a newly-released research paper written with my colleague Charles Martineau. To do so, we build a model where attention-constrained investors rely on equity analysts. In turn, analysts allocate scarce processing power to supply information about different securities.

We find that analysts choose are more likely to focus on stocks already well-covered by their peers. To fix intuition, assume a world where nine analysts cover a “hot” firm, FutureTech, Inc. and no analyst covers SameOld, Inc. The tenth analyst making a coverage choice is better off receiving 1/10th of the attention directed towards FutureTech than becoming the sole forecaster in SameOld. Investors are so limited in their attention that they will choose to read little, if anything, about the less-hyped stock. Coverage begets coverage (in econspeak, we say there are strategic complementarity effects between analysts’ choices).

For investors with very limited attention, coverage crowding is good. A constrained investor cannot learn about too many assets at once, anyway. She has a preference to learn about either riskier assets, where signals are more valuable, or about better covered assets, where signals are easier to get. Therefore, securities with larger fundamental uncertainty (e.g., more intangible assets) are more likely to be crowded. In the figure above, for low attention capacity, the investors’ preferred coverage distribution (in blue) and the equilibrium coverage distribution (in red) coincide.

However, if investors in our model have more attention to spare, they would prefer analyst coverage to be more evenly spread across stocks. Unfortunately, analysts are slow to respond to investors’ preferences. Forecasts become “too crowded,” as analysts choose to join the hype hoping to capture a larger share of investor attention. The resulting inefficiency is driven by a gap between what investors prefer (i.e., to reduce risk on their portfolio) and what analysts want (to get investors’ attention).

More information could, surprisingly, exacerbate the problem. If we introduce better disclosure standards for all stocks, we make them all less risky. Therefore, investors are not so much driven by risk anymore, and would simply prefer easy-to-learn stocks with higher analyst coverage. At the same time, they would neglect stocks with low coverage. From the analysts’ perspective, stepping away from the crowd and covering a “neglected” stock makes less sense in this scenario. As a result, better information could lead to coverage becoming even more crowded.

Our results suggest that analyst coverage clustering is not necessarily benign. Crowding is driven in part by investor demand. However, analysts over-crowd as they have strong incentives to follow the hype as they cannot generate enough interest by “going against the wind.” Big data is unlikely to solve, and may actually aggravate, the problem. The issue is rooted back in our limited capacity to process information.

Paper is available [here].